It is evident that traditional end-to-end business models are breaking down in every industry, including insurance. As the standards of service continue to rise, it becomes increasingly more difficult for any single firm to deliver the seamless digital integration that customers expect. Partnering, then, becomes critical for rapidly developing the flexibility and agility businesses need to stay relevant in today’s hyper-digital world.

The answer to digital disruption in insurance is Ecosystems

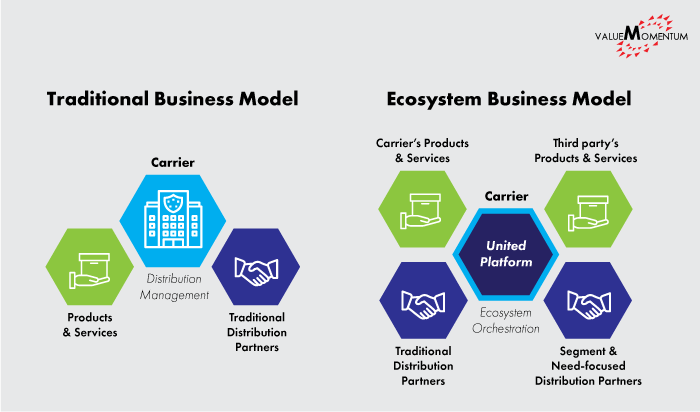

Put simply, insurers must shift towards an ecosystem business model. As opposed to the traditional business model where insurers create and distribute end-to-end products and services, an ecosystem model is characterized by unified digital platforms that incorporate third-party products and solutions, as well as collaboration with segment-focused distribution partners.

To deliver meaningful value, carriers must either bundle value from others with their products (e.g. risk prevention) or provide value to a bundle that someone else is creating (e.g. providing warranty for appliances). To accomplish this, insurers have two major options: (1) Becoming the orchestrator of a micro-ecosystem (2) Becoming a citizen of an existing mega-ecosystem. At the core of both is a symbiotic relationship that allows all parties to capture and deliver more value.

As an orchestrator in the first scenario, insurers must innovate and position themselves at the heart of customer-centric, data-driven ecosystems. Partnering with and leveraging adjacent industries (e.g. Digital Platforms, IoT, AI, blockchain) will allow insurers to deliver integrated value to their customers, and radically transform risk management. Successful orchestrators build out unified platforms or digital platforms that allow them to “orchestrate” the design, development, fulfillment, and service of their own products, as well as those offered by specialist third parties.

In the second scenario, insurers must thoughtfully identify ecosystems they can participate in, and carefully add value to that ecosystem to become a citizen. One example is InsurTech companies that own the Customer Interface segment for an adjacent industry’s ecosystem (e.g. Siemens MindSphere).

In either scenario, data is key. Integrating data with others in the ecosystem will allow custom-integrated solutions, enhanced analytics, and better insights. The value of collaboration will manifest in reduced claims cost, better risk selection and underwriting, better pricing, and new sources of revenue.

Embracing Ecosystems is key to survival in the digital economy

The world is evolving as we speak: new waves of technology or sudden social shifts make it impossible to plan for every emerging need arising from digital disruption in insurance. What matters in the end is the ability to rapidly capture opportunities as they present themselves. An ecosystem-based model enables insurers to cater to micro-segments and-micro needs through a unified platform that optimizes for agile and flexible collaboration with multiple players in the larger ecosystem. Today, success—and survival—are interdependent.

After all, the digital economy is a “made for me” economy. Customers will continue to reward providers who understand and provide the experiences, products, and services they want, as soon as they want it. Streamlined convenience is one half of the equation; speed of innovation is the other. The insurers that can reinvent themselves as key players in the digital ecosystem era will be the insurers that successfully adapt to and survive the seismic disruptions of the digital revolution.

Is your firm prepared to handle the impact of digital disruption in insurance? Learn how you can prepare for and seize the opportunities of the digital era by visiting our Digital & Cloud Services page.